Veterans United Policy Update

Our guidelines have changed regarding a non-purchasing spouse's credit history in a community property state. Currently, Veterans United doesn't consider a non-purchasing spouse's credit score or derogatory credit, including things like collections, foreclosures, bankruptcies, short sales and loan modifications. But we continue to consider the non-purchasing spouse's debts and liabilities, along with judgments or liens.

When it comes time to purchase a home using your VA loan benefits, having a spouse on the mortgage with you can make all the difference. Lenders can count your spouse’s income as long as it's stable, reliable and likely to continue.

But they will also look at the purchasing spouse's debts as well. In some cases, having a spouse with significant debt can have a negative impact on your debt-to-income ratio. If that's your situation, it may be best to proceed solo – even if that means seeking a lower loan amount because you can't count your spouse's income.

Unfortunately, Veterans in nine states don't have the option of simply omitting their spouse's debt, which can make it difficult to qualify for a VA loan. Let's take a closer look at how purchasing in a community property state can complicate the process.

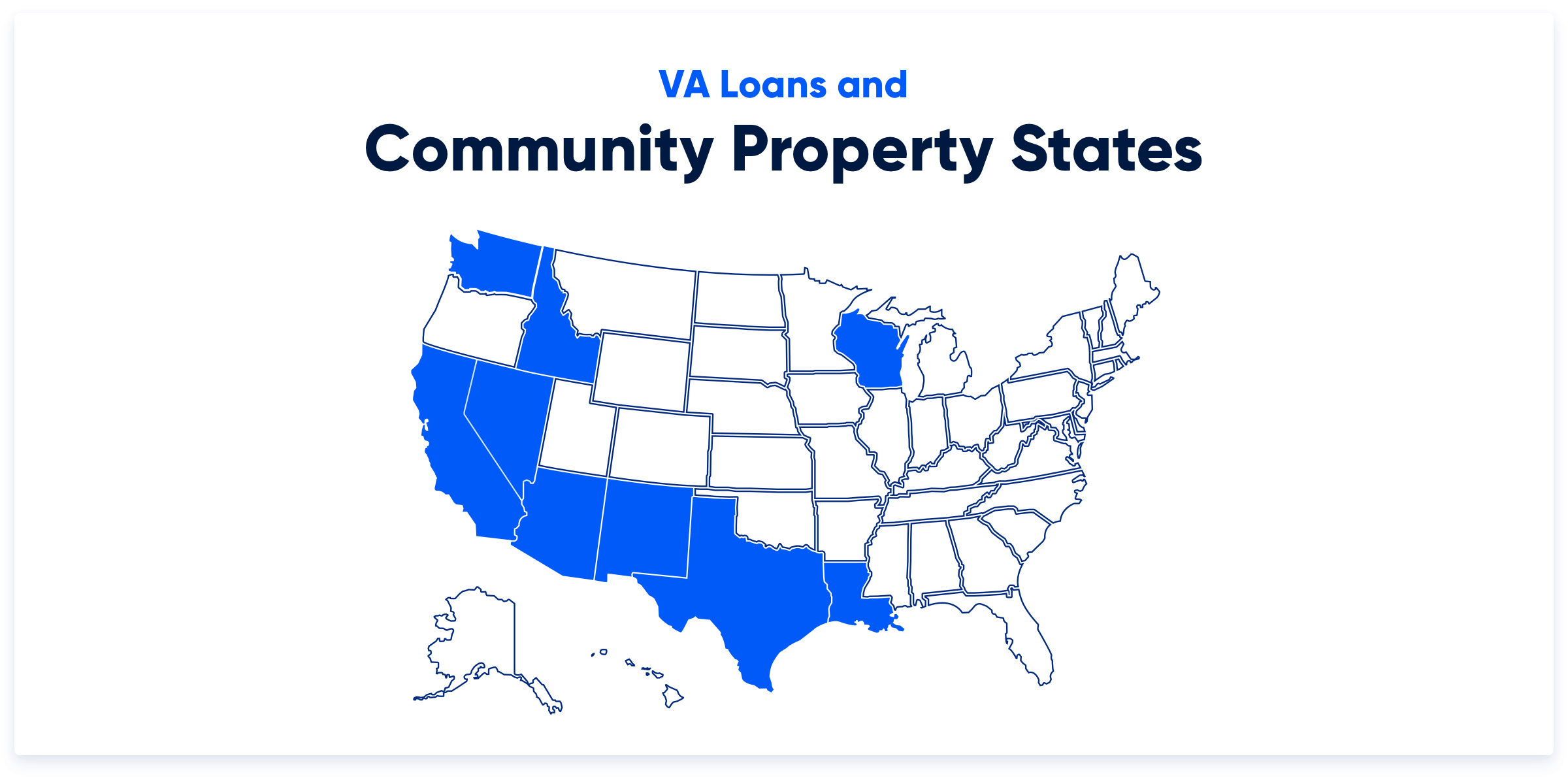

What Are Community Property States?

Community property states require married couples to own property jointly, sharing all assets and debts. The nine states include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin.

How VA Loans Work in Community Property States

In these states, married couples legally share ownership of any property; therefore, any property would be divided upon divorce or other dissolution of the marriage. That adds a layer of potential concern for mortgage lenders, who would otherwise only be concerned with whose name is on the loan.

To counter that, lenders can count the debts of a spouse even if he or she isn't going to be on the mortgage. So even if you have great credit and a healthy debt-to-income ratio, lenders will still take a long, hard look at your spouse's financial profile.

Your spouse's debts will be counted when the lender calculates your DTI ratio. The VA generally wants borrowers to have a DTI ratio of 41 percent or less. If your spouse has any derogatory debt like collections or judgments, that will likely be counted in the lender's derogatory debt cap, which limits the amount of bad debt a borrower can have.

Clearing Up Debt

So is there any way around this for Veterans in community property states?

Some VA lenders may be willing to offset the non-purchasing spouse's debts if he or she has a stable, reliable income that covers them with a little padding left over each month. This is possible but not all too common, mostly because spouses with enough income to cover their debts are typically added to the mortgage as a formal co-borrower.

If you live in one of these nine states and have a spouse with an unhealthy debt load, you may want to prioritize debt repayment and get those levels under control before pursuing a VA home loan.

Related Posts

-

VA Renovation Loans for Rehab & Home ImprovementVA rehab and renovation loans are the VA's answer to an aging housing market in the United States. Here we dive into this unique loan type and the potential downsides accompanying them.

VA Renovation Loans for Rehab & Home ImprovementVA rehab and renovation loans are the VA's answer to an aging housing market in the United States. Here we dive into this unique loan type and the potential downsides accompanying them. -

Pros and Cons of VA LoansAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look.

Pros and Cons of VA LoansAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look.